Last updated on 15th Jul 2020| 2700

What is Cash Flow?

- Cash Flow (CF) is the increase or decrease in the amount of money a business, institution, or individual has. In finance, the term is used to describe the amount of cash (currency) that is generated or consumed in a given time period.

- There are many types of CF, with various important uses for running a business and performing financial analysis. This guide will explore all of them in detail.

Types of Cash Flow

- There are several types of Cash Flow, so it’s important to have a solid understanding of what each of them is.

- When someone refers to CF, they could mean any of the types listed below, so be sure to clarify which cash flow term is being used.

Types of cash flow include:

- Cash from Operating Activities – Cash that is generated by a company’s core business activities – does not include CF from investing. This is found on the company’s Statement of Cash Flows (the first section).

- Free Cash Flow to Equity (FCFE) – FCFE represents the cash that’s available after reinvestment back into the business (capital expenditures). Read more about FCFE.

- Free Cash Flow to the Firm (FCFF) – This is a measure that assumes a company has no leverage (debt). It is used in financial modeling and valuation. Read more about FCFF.

- Net Change in Cash – The change in the amount of cash flow from one accounting period to the next. This is found at the bottom of the Cash Flow Statement.

Uses of Cash Flow

- Cash Flow has many uses in both operating a business and in performing financial analysis. In fact, it’s one of the most important metrics in all of finance and accounting.

The most common cash metrics and uses of CF are the following:

- Net Present Value – calculating the value of a business by building a DCF Model and calculating the net present value (NPV)

- Internal Rate of Return – determining the IRR an investor achieves for making an investment

- Liquidity – assessing how well a company can meet its short-term financial obligations

- Cash Flow Yield – measuring how much cash a business generates per share, relative to its share price, expressed as a percentage

- Cash Flow Per Share (CFPS) – cash from operating activities divided by the number of shares outstanding

- P/CF Ratio – the price of a stock divided by the CFPS (see above), sometimes used as an alternative to the Price-Earnings, or P/E, ratio

- Cash Conversion Ratio – the amount of time between when a business pays for its inventory (cost of goods sold) and receives payment from its customers is the cash conversion ratio

- Funding Gap – a measure of the shortfall a company has to overcome (how much more cash it needs)

- Dividend Payments – CF can be used to fund dividend payments to investors

- Capital Expenditures – CF can also be used to fund reinvestment and growth in the business

Cash Flow VS Income

- Investors and business operators care deeply about CF because it’s the lifeblood of a company.

- You may be wondering, “How is CF different from what’s reported on a company’s income statement?” Income and profit are based on accrual accounting principles, which smooths-out expenditures and matches revenues to the timing of when products/services are delivered.

- Due to revenue recognition policies and the matching principle, a company’s net income, or net earnings, can actually be materially different from its Cash Flow.

- Companies pay close attention to their CF and seek to manage it as carefully as possible.

- Professionals working in finance, accounting, and financial planning & analysis (FP&A) functions at a company spend significant time evaluating the flow of funds in the business and identifying potential problems.

Below are the steps involved in capital budgeting.

- Identify long-term goals of the individual or business.

- Identify potential investment proposals for meeting the long-term goals identified in Step 1.

- Estimate and analyze the relevant cash flows of the investment proposal identified in Step 2.

- Determine financial feasibility of each of the investment proposals in Step 3 by using the capital budgeting methods outlined below.

- Choose the projects to implement from among the investment proposals outlined in Step 4.

- Implement the projects chosen in Step 5.

- Monitor the projects implemented in Step 6 as to how they meet the capital budgeting projections and make adjustments where needed.

There are several capital budgeting analysis methods that can be used to determine the economic feasibility of a capital investment. They include the Payback Period, Discounted Payment Period, Net Present Value, Profitability Index, Internal Rate of Return, and Modified Internal Rate of Return.

Cash Flow Generation Strategies

- Since CF matters so much, it’s only natural that managers of businesses do everything in their power to increase it.

- In the section below, let’s explore how operators of businesses can try to increase the flow of cash in a company.

- Below is an infographic that demonstrates how CF can be increased using different strategies.

- Managers of business can increase CF using any of the levers listed above.

- The strategies for improving CF fall into one of three categories: revenue growth, operating margins, and capital efficiency.

- Each of those can then be broken down into higher volume, higher prices, lower cost of goods sold, lower SG&A, more efficient property plant & equipment (PP&E), and more efficient inventory management.

Learn On-Demand Blockchain Certification Course from Certified Blockchain Experts

Weekday / Weekend BatchesSee Batch DetailsFeatures of Capital Budgeting:

- Capital Budgeting involves potentially large anticipated benefits.

- Its involves a high degree of risk due to high cash outlay and planned for a longer period.

- It also involves a long gestation period between the initial outlay and the anticipated return.

Capital Budgeting Process

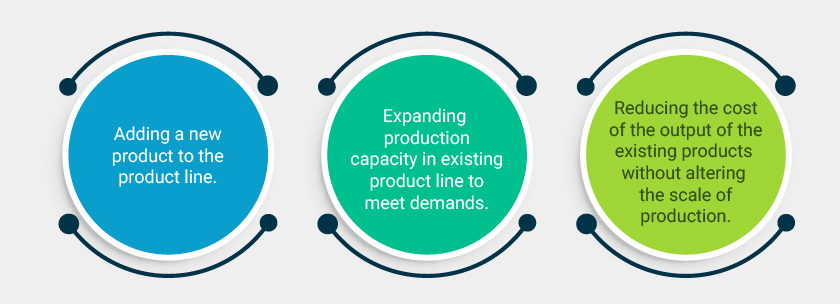

Project Generation

Generating a proposal for investment is the first step in the capital budgeting process. The proposal may fall into one of the following categories.

Project Evaluation

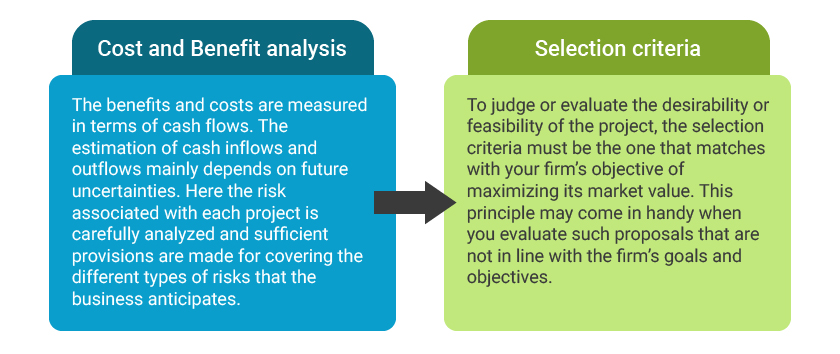

It is the crux of capital budgeting where a project undergoes cost-benefit analysis considering the risks and future uncertainties associated. It generally involves two-step analysis.

Project Selection

There is no standard administrative procedure to guide the management to select the best project among the bests or approving a correct investment proposal. The screening and selection procedures for selecting a project differ from firm to firm.

Acquiring funds for the project

Once a project proposal is finalized by the management or the management agrees with the capital expenditure for the project, the finance manager then explores the different alternatives available for acquiring the funds.

The manager then prepares the capital budget with an approach to reduce the average cost of funds so that the project is available for selection or attracts the interest of the management.

He also prepares a periodical report which helps in reviewing the performance of the projects which will help the management to make informed decisions throughout the project’s lifetime, and even after completion when they go for another project with the same selection criteria.

Follow up proposal

In the follow-up proposal, comparison of actual performance with original estimates is carried out. It not only ensures better forecasting but also helps in sharpening the techniques for improving future forecasts.

Major capital projects involving huge amounts of money, as well as capital expenditures, can get out of control quite easily if mishandled and end up costing an organization a lot of money. However, with effective planning, the right tools, and good project management, that doesn’t have to be the case.

Capital Budgeting Examples and Calculations

Example -1

- Max limited is looking to invest in a new project and the cost of the project is Rs. 12,000 /-. Before investing, they want to analyze that how long it will take to recover invested money in a project?

- Estimated profit for first and the subsequent year is given below:

| Year | Profits ( Amount in Rs. ) |

|---|---|

| First Year | Rs. 3,000 |

| Second Year | Rs. 3,000 |

| Third Year | Rs. 3,000 |

| Fourth Year | Rs. 3,000 |

- Looking at the above table, one can make out that a company can recover the invested money in 4 years. But this is not the right way to find out a payback period of the initial investment. Here, the company is considering profit and not the net cash flows. In order to arrive at the payback period, you should use net cash flow.

- As we know that profit is arrived after deducting depreciation and other non-cash expenses, so to know the correct net cash flows, we must add depreciation and other non-cash expenses to profits.

Let’s say depreciation value is Rs. 2,000 /-

- The net cash flow after considering deprecation is given below:

| Year | Profits (Amount in Rs. ) | Depreciation | Cash flows before Depreciation | Cumulative Cash flows |

|---|---|---|---|---|

| First Year | Rs. 3,000 | Rs. 2,000 | Rs. 5,000 | Rs. 5,000 |

| Second Year | Rs. 3,000 | Rs. 2,000 | Rs. 5,000 | Rs. 10,000 |

| Third Year | Rs. 3,000 | Rs. 2,000 | Rs. 5,000 | Rs. 15,000 |

| Fourth Year | Rs. 3,000 | Rs. 2,000 | Rs. 5,000 | Rs. 20,000 |

- From the above analysis, a company will recover the initial investment in 2 years and few months. To arrive exact payback period, the following formula can be used:

- Payback period = Investment Required/ Net Annual Cash Flow

12,000/5,000 =2.4 years

- Here, the payback period is nothing, but the time taken to recover the investment amount. The above payback period can be applied if the annual net cash flow is even. In case of uneven net cash flow, the calculation applied in below example can be used.