Last updated on 16th Oct 2025| 10418

- What is Management Accounting?

- Process of Management Accounting

- Objectives

- Key Functions

- Budgeting and Forecasting

- Cost Analysis Types & Techniques

- Performance Measurement

- Decision-Making Support

- Tools and Techniques

- Advantages and Challenges

- Conclusion

What is Management Accounting?

Management accounting plays a pivotal role in internal financial management, helping organizations achieve their strategic and operational goals. While financial accounting is concerned with external reporting to stakeholders like investors and regulators, management accounting is focused on providing information to internal stakeholders, particularly managers. This allows them to make informed decisions that drive business performance. To bridge the gap between financial insights and strategic execution, explore Business Analyst Training a Chennai-based program designed to equip professionals with analytical tools, data interpretation skills, and decision-making frameworks essential for driving organizational growth. The dynamic and evolving business environment has made management accounting indispensable for organizations seeking to maintain competitive advantage and achieve long-term growth. Management accounting serves as a decision-support tool that helps managers plan, control, and optimize business operations. It involves the collection, analysis, and reporting of financial and non-financial information to aid in decision-making processes. As businesses continue to face economic volatility and competition, management accounting has become an essential practice for sustaining operational efficiency and fostering innovation.

Process of Management Accounting

Management accounting is the process of preparing management reports and accounts that provide accurate and timely financial and statistical information. This information helps managers to make day-to-day and short-term decisions to meet the organization’s objectives. Unlike financial accounting, which is governed by external standards such as Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS), management accounting is more flexible and tailored to the specific needs of an organization’s leadership. To strengthen these decision-making capabilities with data-driven insights, explore Learn Business Analytics a practical guide to mastering analytical tools, interpreting performance metrics, and aligning business strategies with measurable outcomes. It combines both financial and non-financial data to assist managers in planning and controlling operations. Management accountants analyze costs, revenues, and performance to provide insights that enable managers to make informed decisions about resource allocation, budgeting, and financial forecasting.

Interested in Obtaining Your Business Analyst Certificate? View The Business Analyst Training Offered By ACTE Right Now!

Objectives

The main objectives of management accounting are: providing timely and relevant information to support internal decision-making, optimizing resource allocation, and improving operational efficiency. To understand how different analytical roles contribute to these goals, explore Business Analyst vs Data Analyst a comparative guide that breaks down the distinct responsibilities, skill sets, and strategic impact of each role within modern organizations.

- Facilitating Planning and Forecasting: Management accounting supports organizations in creating strategic and operational plans. These plans provide a roadmap for achieving business goals. It also helps in forecasting future financial performance based on historical data and trends, ensuring that the business is prepared for different scenarios.

- Assisting in Decision Making: Management accounting aids managers in making informed decisions. It provides them with data that highlights the financial implications of various business choices, such as pricing, cost-cutting, and investment decisions.

- Enhancing Control: One of the key objectives of management accounting is to ensure that the organization’s resources are used efficiently and effectively. This is achieved through monitoring actual performance against budgets or standards, identifying variances, and taking corrective actions where necessary.

- Evaluating Performance: Management accounting evaluates the performance of departments, products, and personnel. This is done by comparing actual performance with pre-established targets or benchmarks. Such evaluations help in identifying areas for improvement and setting new performance goals.

- Resource Optimization: By analyzing costs and revenues, management accounting helps managers make informed decisions about resource allocation. This ensures that the organization’s resources, such as labor, capital, and materials, are utilized in the most efficient manner.

- Improving Communication: Timely and relevant financial information enables effective communication between managers, teams, and departments. Management accountants provide the necessary insights to stakeholders within the organization, helping them understand financial conditions and goals.

- Planning: Management accountants assist in creating both short-term and long-term plans for achieving business objectives. These plans include budgeting, financial forecasting, and strategic goals.

- Controlling: Control refers to the process of ensuring that the organization’s operations stay on track to achieve set goals. Management accountants help monitor financial performance and analyze variances to take corrective action where necessary.

- Decision Making: Managers rely on management accountants for data-driven insights that guide decisions. This includes making decisions on investments, cost control, product pricing, and resource allocation.

- Financial Reporting: Management accounting involves the creation of reports that help internal stakeholders track the financial health of the organization. These reports include income statements, balance sheets, and cash flow statements tailored to internal management needs.

- Risk Management: Management accountants help identify financial risks, assess their potential impact, and recommend strategies to mitigate those risks.

- Performance Evaluation: Management accounting evaluates the efficiency of operations and the effectiveness of various departments or individuals. It uses various performance metrics, including KPIs, to assess progress toward achieving goals.

- Fixed Costs: These costs remain constant, regardless of the level of production or activity. Examples include rent, salaries, and depreciation.

- Variable Costs: These costs fluctuate with the level of production. For instance, raw materials, direct labor, and utilities vary depending on output.

- Semi-variable Costs: These costs have both fixed and variable components. For example, utility costs may have a fixed monthly fee plus charges based on usage.

- Break-even Analysis: This technique calculates the sales volume at which total revenue equals total costs, helping to identify the point at which the company starts making a profit.

- Marginal Costing: Marginal costing helps businesses analyze the additional cost of producing one more unit of a product. This analysis aids in pricing decisions and profitability analysis.

- Standard Costing: Standard costing compares actual costs with predetermined costs (standards). This method highlights variances, which can indicate areas where performance needs improvement.

- Make or Buy Decisions: When considering whether to make a product in-house or outsource its production, management accountants analyze the cost implications and potential impact on quality and delivery.

- Pricing Decisions: Management accounting supports pricing strategies by analyzing costs, market demand, and competitive factors. Proper pricing ensures profitability while staying competitive in the market.

- Product Mix Decisions: Management accountants assess the profitability of different products or services to determine the optimal product mix that maximizes revenue.

- Capital Investment Decisions: For large investments, management accountants use techniques like Net Present Value (NPV) and Internal Rate of Return (IRR) to evaluate the potential return on capital expenditure.

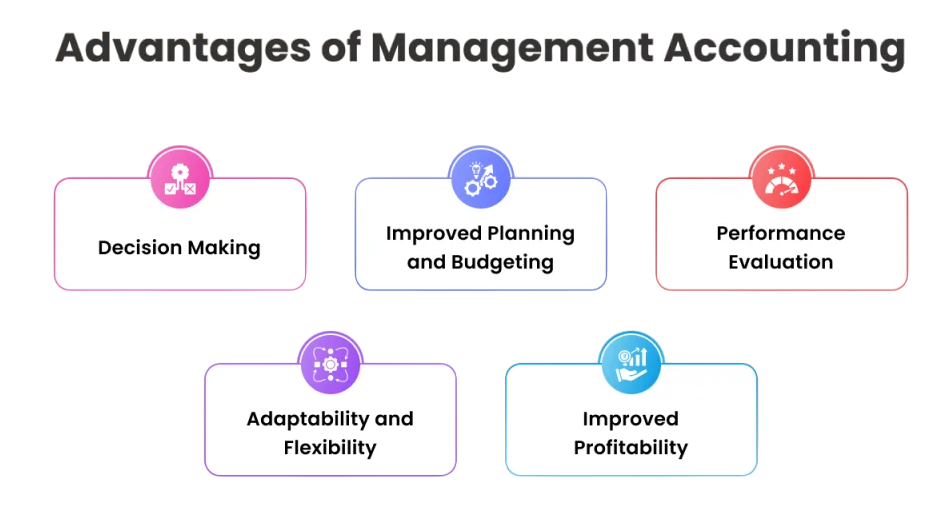

- Informed Decision-Making: Management accounting provides data-driven insights that help managers make informed decisions on pricing, investments, and resource allocation.

- Operational Efficiency: Helps in identifying cost-saving opportunities and optimizing resource utilization.

- Strategic Alignment: Ensures that financial planning is aligned with organizational goals.

- Flexibility: Allows organizations to tailor reports to specific management needs.

- Proactive Management: Helps managers anticipate challenges and mitigate potential risks before they affect business performance.

- Data Overload: Too much information can overwhelm decision-makers and obscure key insights.

- Implementation Costs: Advanced tools and systems can require significant investment.

- Resistance to Change: Employees may resist new accounting processes, especially if they are unfamiliar with the technology or techniques involved.

- Skill Requirements: Management accounting requires specialized knowledge and expertise in financial analysis and reporting.

- Lack of Standardization: The flexibility of management accounting means that reports may lack consistency across organizations or departments.

To Earn Your Business Analyst Certification, Gain Insights From Leading Data Science Experts And Advance Your Career With ACTE’s Business Analyst Training Today!

Key Functions

Management accounting encompasses various functions that contribute to the decision-making process. These functions include budgeting, forecasting, performance evaluation, and cost management. To align these financial insights with technology-driven process improvements, explore Business Systems Analyst a role that bridges the gap between business objectives and IT solutions by analyzing workflows, optimizing systems, and ensuring data-driven decision support.

E-commerce and digital connectivity have removed traditional barriers. Local products can now compete globally.

Develop Your Skills with Business Analyst Online Training

Weekday / Weekend BatchesSee Batch DetailsBudgeting and Forecasting

Budgeting in management accounting is one of the most essential financial planning tools that give organizations a complete outline of their income, expenses, and cash flows for the future. Different budget types like operational, capital, and cash budgets help companies to effectively manage their financial position. Operational budgets are used to control daily activities, while capital budgets are used to plan for the future investments in machinery and property. Cash budgets are very important in the provision of sufficient cash to meet short-term obligations. Forecasting, which is used alongside budgeting, allows a company to make a decision in advance by giving a prediction of the future business results based on past data and market trends. To turn these financial insights into a strategic career advantage, explore How to Become a Business Analyst a step-by-step guide that outlines the skills, certifications, and practical experience needed to transition into a role that bridges data, strategy, and decision-making. Besides, cost analysis is the main part of management accounting that gives the authority to the managers to assess the financial effects, have control over the expenditures and recognize the possibilities for increasing the profit margin. By using these interrelated financial measures, a firm can build up strong financial management practices that are able to initiate strategic growth and stable performance.

Want to Pursue a Business Analyst Master’s Degree? Enroll For Business Analyst Master Program Training Course Today!

Cost Analysis Types & Techniques

Cost Analysis Types

Cost Analysis Techniques

Go Through These Business Analyst Interview Questions and Answers to Excel in Your Upcoming Interview.

Performance Measurement

It is very important to measure the performance of an organization in order to figure out the areas where the company is inefficient and to make the necessary changes. Management accounting uses very complex techniques such as Return on Investment (ROI) which is used to measure the profitability of investments by comparing the financial returns to the initial costs. Along with ROI, Economic Value Added (EVA) reveals even more details about the worth of a business in the long term by calculating the net income that exceeds the minimum capital requirements. To translate financial metrics into actionable insights and strategic decisions, explore Business Analyst Training a program designed to equip professionals with analytical frameworks, data interpretation skills, and business acumen essential for driving long-term value creation. Moreover, the Balanced Scorecard, a performance evaluation tool, goes beyond financial measures by looking at non-financial aspects such as customer satisfaction, internal processes, and employee skills. By making use of these all-inclusive performance measurement instruments managers obtain the opportunity to systematically monitor progress, decide on strategic changes based on data and create a clear system of accountability amongst organizational teams which, ultimately, leads to the establishment of a culture of continuous improvement and strategic alignment.

Decision-Making Support

Management accounting provides critical data for decision-making, including budgeting, forecasting, performance tracking, and cost analysis. To integrate these functions into a structured analytical workflow, explore Business Analytics Process Model a lifecycle framework that guides how data is collected, processed, analyzed, and translated into actionable insights for strategic and operational decisions.

Tools and Techniques

Management accounting uses advanced instruments and methodologies to accomplish strategic decision-making and to make the operational level more efficient. The Activity-Based Costing (ABC) System gives a more detailed viewpoint of the allocation of the overhead by showing what the actual cost of the products or services is. Variance analysis is an instrument for detecting deviations of actual financial performance from the plan by comparing these two and, consequently, it is very useful in obtaining a corrective action. To complement this with structured frameworks for identifying root causes and implementing solutions, explore Business Analyst Methodologies a resource that outlines proven techniques for diagnosing performance gaps, aligning stakeholder expectations, and driving continuous improvement through data-informed strategies. Cost-Volume-Profit (CVP) analysis, in this way, can be simply utilized by managers so as to have a greater insight into intricate relationships between cost, volume, and profitability, and therefore to be able to make more accurate pricing and budgeting decisions. Throughput Accounting is, therefore, one of the methods which, together with these, can be used by the company to improve its results by focusing on revenue generation through process optimization and bottleneck reduction. Strategically, companies can also take advantage of benchmarking as a comparative tool. With it, they can, for example, evaluate efficiency, identify opportunities and, as a result, improve their competitive position and increase profits.

Advantages and Challenges

Advantages

Challenges

Conclusion

Management accounting is an essential practice for modern organizations. It equips managers with the tools and insights they need to plan, control, and optimize business operations. As organizations continue to navigate complex and competitive business environments, the role of management accounting will only grow in importance. To complement financial expertise with strong communication, strategic thinking, and leadership capabilities, explore Softskills Training a placement-focused program designed to equip professionals with the interpersonal skills needed to influence decisions, collaborate across departments, and drive organizational success. By supporting decision-making, performance evaluation, and strategic alignment, management accounting contributes significantly to the achievement of organizational objectives and the sustainable growth of businesses.